2019 Real Estate Outlook

- Admin

- Jan 7, 2019

- 3 min read

Updated: Jan 14, 2019

The "Wind" and the "Charts" (click on photo)

We have been reviewing many sources for opinions on how the market should perform this year. There are differences of opinion, but we combined the information with our street knowledge. Here is what we believe to be expected.

The “Wind” – there is never ending news about trade wars, the wall, stock market, etc., expect most issues will eventually be resolved. But, while unemployment is very low and most businesses are thriving, there are growing concerns about where things are headed. Issues of most importance that can derail any forecast: Global Growth slowing, high Bond prices not reflective of actual value, stock market and housing market at highs and poised for a correction. Whether it is a sudden strong "Wind" of change or gradual, the timing is unknown.

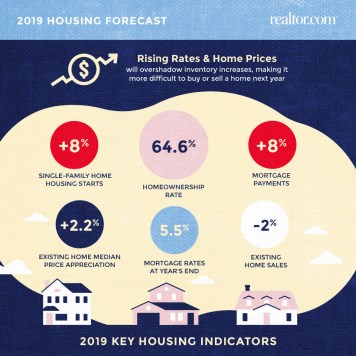

The Charts – looking at factual market information is important (it’s not fake news). What the Charts show for 2018:

The # of sales and closed sales have been declining (low inventory).

Conversely, average sales price continued to rise. In Chicago, as of Nov 2018 reporting, Single Family Homes rose 4.0% and Condos 6.7%. However, when the December figures are released, we expect to see declines in year over year #'s.

For the greater Chicago Area, the median sales price was up about 4.0%.

Buyer’s don’t like low inventory (fewer choices) combined with higher prices, so many hesitated about making a purchase, preferring a wait-and-see position.

Our Opinion for 2019

Expect the # of properties coming to market to increase, a moderate 7%.

The median sales price increase will slow, perhaps within the 2.2% - 2.5% range.

Buyers will have more options and feel more confident to make a purchase.

First 4-6 months should favor sellers, then a gradual shift to a more balanced market.

Summary: Although it remains a seller’s market, sellers will need to be mindful of their increasing competition and shouldn’t necessarily expect to name their price and get it in full — a change from the past few years. Above-median priced sellers, may find it will take longer to sell and require offering incentives, such as price reductions or closing credits. There will be fewer bidding wars and multiple offers. However, with inventory expected to remain limited in most markets, sellers who price competitively can still achieve top dollar with a short time on the market, but not the price jumps observed in previous years.

What to Watch: There are many properties that did not sell in 2018. In the first full week of Jan 2019 we already see a trend - properties being relisted now with price reductions (some very significant) and brand new listings already for sale. We'll have to watch if there is a "wave" of properties coming to market and if this changes the overall dynamics. The support components of the economy will be critical to watch each month, if there is a correction it will affect everything.

For Sellers

The beginning of a new year and season brings out many buyers. The first 4-6 months will be the best time to sell to achieve the highest price. The market starts now and every week will have an increasing # of properties coming to market. Also, as a seller it is prudent to understand the “A”, “B”, “C”s

A – Hot property: best location, excellent condition, priced to sell, will get offers right away.

B – Good property: good location, condition and pricing – may take 30-60 days to get offers.

C – Needs help property: not the best location, condition or pricing – Your prospects for selling may take longer, but if you price appropriately in the beginning, you can be successful. Remember – real estate is not based on what you “want” or “need”, but rather what similar properties have sold for.

Potential Opportunities As mentioned in a Chicago Tribune article – “...generational turnover is accelerating, as the oldest baby boomers finally relinquish their houses… That translates to a bumper crop of split-levels and ranch houses that can be renovated to the open-concept layouts popular with young families."

Note: Real Estate is very property specific, certain segments perform better than others. Example: The North / Northwest side homeowners were the most “equity rich”, while many Southside homeowners still seriously “underwater”.

Sources reviewed: Realtor.com, Illinois Realtors Assoc., Case Schiller, Zillow and Chicago Tribune.

Best Wishes in 2019

“Be Genuine”

Comments